Seldom has one man received so much credit and done so little to deserve it. Alan Greenspan's last day on the job is tomorrow, January 31, 2006.

I am certain the central bankers have found another person who will not threaten them in new Fed chairman Ben Bernanke. I am even more certain they have found a person with more integrity.

No single person exercises more control over the economy than the chairman of the Federal Reserve with his control over monetary policy. Greenspan was not elected and he didn't need a spotless private life, yet he held office through four administrations, Democrat and Republican. He maintained office simply on the reputation of being an inflation hawk, a reputation he built and maintained to the detriment of millions of Americans.

A great deal of credit for his appointment and longevity goes to his skill in cultivating the power elite. As described in Bob Woodward's book Maestro, few couples are more prominent on the A-list social scene in the nation's capitol than the Fed chairman and his wife NBC White House correspondent Andrea Mitchell.

Perhaps less surprising, but surprising nonetheless, is the portrayal of Greenspan as a master manipulator of the bureaucracy at the Fed. More than one governor has quit in frustration at being unable to influence policy.

As familiar as Greenspan's coke bottle glasses and his deeply furrowed face is his manner of speaking, an obfuscating and convoluted style that he apparently inherited from his father. It goes with him wherever he goes. He is said to have proposed marriage twice to Mitchell before she accepted. She had not understood the first time.

Let's hear it in his own words.

"Economic conditions and considerations addressed by the committee are essentially the same as when the committee met in February. The committee remains concerned that increases in demand will continue to exceed the growth in potential supply, which could foster inflationary imbalances that would undermine the economy's record economic expansion."

That was from March 2001. Seems to make sense in a way, "inflationary imbalances" is kind of a odd way of saying inflation, perhaps. Except there was no inflation. There was never any inflation. The statement accompanied a quarter point hike in the federal funds rate.

Skip ahead a year.

"Our accelerated action reflected the pronounced downshift in economic activity, which was accentuated by the especially prompt and synchronous adjustment of production by businesses utilizing the faster flow of information coming from the adoption of new technologies."

This was accompanied by a lowering of the federal funds rate. It should have read, "I screwed up big time."

Between those two pronouncements, Greenspan's stock tumbled as far as that of any of the dot.com start-ups. Once revered as the architect of permanent prosperity, Greenspan was then blamed for an unnecessary slump, before he was forgotten in the fallout from the tragedy of 9-11. That event, in fact, caught him in Europe where he was begging the EU central banks to lower their interest rates to bail out the economy. He was locked out of the country for three days when air travel was shut down.

Both Greenspan and Bush later took advantage of the terrorist attacks to excuse the subsequent economic downturn. In the past, wars have been identified as good for the economy. This time they were just good for cover.

Let's go over it again. At the beginning of 1999 the American economy was booming, the stock market was booming, help wanted signs were everywhere. The U.S. had barely paused on its upward trajectory as Russia defaulted on its bonds and Asian currencies melted down. We were invulnerable.

Then Alan Greenspan saw inflation in the tea leaves, or said he did, and the Fed began to ratchet up interest rates. Wall Street scratched its collective head. What inflation? The only thing on the horizon was the 2000 presidential election. By the time he stopped, the prime rate stood at 9.5 percent. In real terms it was the highest since the Reagan/Volcker recession of 1981.

The worst of it was that it occurred at the same time as a rise in oil prices and an explosion in energy costs, definite drags on an economy which certainly did not need the additional burden of higher interest rates. Too late, the Fed found out that it was much easier to stop an economy with monetary policy than it is to restart one. The prime rate sat at post-war lows for more than two years, and the recovery is still doubtful.

Prior to its occurrence I would have bet large amounts of money that George W. Bush would not reappoint Greenspan for his last four-year term. W's father, H.W., was no great friend of Greenspan's, blaming him for the slowdown in 1991 which hurt his reelection chances. The elder Bush is quoted as saying, "I reappointed him and he disappointed me."

My amazement wore off quickly when Greenspan strode into Congress and said the budget surplus was a threat to our nation's future. Without support from this so-called economic genius, the Bush tax cuts would likely never have come into being. I posted the nonsensical reasoning last month.

His chairmanship of the Social Security Commission in the early 1980s that raised payroll taxes with the promise of putting Social Security on firm financial footing has been completely discredited by his contributions to the undermining of fiscal integrity in the federal budget, in concert with George W. Bush, and its inevitable toll on the entitlement funds.

As he retires, Greenspan can look out on a sea of red ink, both federal deficits and private debt, and count it as his legacy. He can point to his contribution in keeping the dollar overpriced and thus our trade deficits high. He can say with confidence that he has reduced the Fed's tools for affecting the economy to one, the federal funds rate. Maestro Magoo can know with confidence that he operated in a manner consistent with retaining his job and consistent with nothing else.

Monday, January 30, 2006

Monday, January 30, 2006

Sunday, January 29, 2006

"Fat Boy," "Death Star" and "Lucky Dub"

George Bush's spiritual brethren at Enron will finally go on trial. Jury selection begins tomorrow in a Houston federal court. The headliners were once Kenneth Lay, Jeff Skilling, and Rich Causey, but Causey, formerly Enron's top accountant, turned state's evidence. Attorneys for the other two tried unsuccessfully to get a further delay, saying a fair trial in Houston (remember "Enron Field") was not possible. Eighty percent of citizens there have a negative view of the gentlemen.

These are George Bush's fellow travellers, not only because "Kenny Boy" Lay and other Enron insiders were among his buddies and prime political backers, but more so because Enron-type fraud was Dubya's preferred MO. Tom DeLay and Jack Abramoff are into low-brow graft next to Bush and corporate cooking of the books.

One mode of corporate fraud, the "fictitious asset sale," was beneficial to both Bush and Enron. Company A sells its asset to Company B at an enormous price, adds the gains to profits, wows the market with the balance sheet, sells a lot of high priced stock, and hopes nobody finds out that Company B was just Company A under another name and the asset was worth a fraction of the sale price.

Details: The story was recounted by Paul Krugman in the July 2, 2002, NYT. In 1989 George had gotten on the board of Harken Energy when Harken bought his tiny, money-losing, highly indebted company Spectrum 7 for $2 million ("because his name was George Bush"). Harken was losing money too, but was able to hide its losses with profits generated by the sale of an asset, its subsidiary Aloha Petroleum. Eventually the SEC ruled the transaction to be phony because the purchasers of Aloha were simply a group of Harken insiders (who had, in fact, borrowed much of the money from Harken itself).

Before the stock tanked, Mr. Bush sold off two-thirds of his share, $848,000 worth, and in spite of insider trading laws requiring prompt disclosure, neglected to inform the SEC for 34 weeks. An internal SEC memorandum concluded that he had broken the law. No charges were filed. Daddy was president.

The rest of Bush's business career reeks as well. The proceeds from Harken were invested in the Texas Rangers baseball club, and after "an equally strange story," as Krugman puts it, George became a truly rich man.

So when we relive the Enron market-rigging scandal, think not only of "Fat Boy," "Death Star," and "Get Shorty," but also of "Lucky Dubya." They've all cost us dearly.

These and other stories from his NYT columns were collected in Krugman's best-selling book The Great Unraveling: Losing our Way in the New Century. Krugman is an object lesson in why economists speak of things with the term "relative." Today he is viewed by all as definitely on the left, but during the first part of his career the economist was so much in the center you might have called him "apolitical." It wasn't Krugman who changed position, it was the rest of the landscape that moved to the right.

Footnote: Son of Enron. The New York Stock Exchange welcomed Refco, a commodities broker, in August. Refco stock spiked 25 percent. In October its CEO Phillip Bennett was arrested for fraud when it was found that $430 million in debt had been kept off the books. A week later Refco filed for bankruptcy.

These are George Bush's fellow travellers, not only because "Kenny Boy" Lay and other Enron insiders were among his buddies and prime political backers, but more so because Enron-type fraud was Dubya's preferred MO. Tom DeLay and Jack Abramoff are into low-brow graft next to Bush and corporate cooking of the books.

One mode of corporate fraud, the "fictitious asset sale," was beneficial to both Bush and Enron. Company A sells its asset to Company B at an enormous price, adds the gains to profits, wows the market with the balance sheet, sells a lot of high priced stock, and hopes nobody finds out that Company B was just Company A under another name and the asset was worth a fraction of the sale price.

Details: The story was recounted by Paul Krugman in the July 2, 2002, NYT. In 1989 George had gotten on the board of Harken Energy when Harken bought his tiny, money-losing, highly indebted company Spectrum 7 for $2 million ("because his name was George Bush"). Harken was losing money too, but was able to hide its losses with profits generated by the sale of an asset, its subsidiary Aloha Petroleum. Eventually the SEC ruled the transaction to be phony because the purchasers of Aloha were simply a group of Harken insiders (who had, in fact, borrowed much of the money from Harken itself).

Before the stock tanked, Mr. Bush sold off two-thirds of his share, $848,000 worth, and in spite of insider trading laws requiring prompt disclosure, neglected to inform the SEC for 34 weeks. An internal SEC memorandum concluded that he had broken the law. No charges were filed. Daddy was president.

The rest of Bush's business career reeks as well. The proceeds from Harken were invested in the Texas Rangers baseball club, and after "an equally strange story," as Krugman puts it, George became a truly rich man.

So when we relive the Enron market-rigging scandal, think not only of "Fat Boy," "Death Star," and "Get Shorty," but also of "Lucky Dubya." They've all cost us dearly.

These and other stories from his NYT columns were collected in Krugman's best-selling book The Great Unraveling: Losing our Way in the New Century. Krugman is an object lesson in why economists speak of things with the term "relative." Today he is viewed by all as definitely on the left, but during the first part of his career the economist was so much in the center you might have called him "apolitical." It wasn't Krugman who changed position, it was the rest of the landscape that moved to the right.

Footnote: Son of Enron. The New York Stock Exchange welcomed Refco, a commodities broker, in August. Refco stock spiked 25 percent. In October its CEO Phillip Bennett was arrested for fraud when it was found that $430 million in debt had been kept off the books. A week later Refco filed for bankruptcy.

Saturday, January 28, 2006

Economists "oops" day

Maybe there was something to that interest rate inversion stuff. Commerce Department numbers released Friday show GDP growth back down to 2003 levels, at 1.1% and falling.

The Economic Policy Institute (EPI) snapshot depicts slow growth across the board, not just in autos. Growth in consumption, business investment, residential investment, and exports all fell from the third quarter into the fourth quarter. Final sales of domestic output actually shrank in absolute terms.

An earlier EPI piece showed that federal tax cuts have produced no new jobs. Forget the happy talk. Employment growth was generated not in the private economy from tax cuts, but came from new government spending. Jobs from Defense-related and discretionary spending was estimated at 2.82 million between 2001 through the end of 2006. Total job growth, as above, was only 2.0 million. Jobs generated by the tax cuts have actually declined the difference of 820,000. This in spite of the rock bottom interest rate regime the Fed has been following until recently.

Without job growth, there is no possibility of overall economic growth. Even the total of 2 million jobs over five years is fewer than Bill Clinton averaged every single year of his presidency, while shrinking the deficit.

What does this mean?

The Bush tax cuts have produced less than nothing. The economy is weaker for the effort. This is because those cuts have been targeted to the rich. The rich don't spend out of new income such as they get from tax refunds, but rather out of accumulated wealth.

It also means George Bush does not know what he is doing. Wait, you say, Dubya knows exactly what he is doing -- He is operating fiscal policy for the benefit of his rich corporate buddies. Fair point. What Bush does not know is that in the process he is killing the economy for everyone and choking off any possibilities for a rebound with big new debt.

He invaded Iraq with a purpose, too, but without understanding reality or the ramifications of his adventure. He and his Neocon ditto tank have produced a situation without an answer in the Middle East. They may have done the same thing with the domestic economy.

As Robert Rubin pointed out last week, the US -- alone among industrial nations -- has combined huge federal deficits and stagnant incomes with a very low personal savings, high personal debt and enormous trade deficits.

Yes, I am the voice of doom and gloom. It may surprise you that the economy of these posts is different than that witnessed to by the talking heads. It surprises me as well. Economics is not in the height of its glory right now, but surely we can do better than the line by Laurence J. Peter: "An economist is an expert who can explain precisely tomorrow why the things he predicted yesterday didn't happen today."

Most of the problem is politicization, both internal academic politics and the Heritage Foundation style. A new report from scientists at Emory University studied committed political partisans with MRIs. They discovered that reasoning centers in the brain were quiescent during the process of evaluating politically charged material, but circuits lit up that are connected with emotion and resolving conflicts. When acceptable conclusions were reached -- often by suppressing or ignoring difficult information -- circuits associated with behavior reward came on line. "Much like that seen when addicts get a drug," according to Drew Westen, director of clinical psychology at Emory. (See "Partisans don't let the facts get in the way of the truth.")

If you've ever seen economists argue, you know this is what is happening. Entire schools are built on logical flaws or assumption errors, supported only by vigorous debate and polemics. Very much too bad.

The Economic Policy Institute (EPI) snapshot depicts slow growth across the board, not just in autos. Growth in consumption, business investment, residential investment, and exports all fell from the third quarter into the fourth quarter. Final sales of domestic output actually shrank in absolute terms.

An earlier EPI piece showed that federal tax cuts have produced no new jobs. Forget the happy talk. Employment growth was generated not in the private economy from tax cuts, but came from new government spending. Jobs from Defense-related and discretionary spending was estimated at 2.82 million between 2001 through the end of 2006. Total job growth, as above, was only 2.0 million. Jobs generated by the tax cuts have actually declined the difference of 820,000. This in spite of the rock bottom interest rate regime the Fed has been following until recently.

Without job growth, there is no possibility of overall economic growth. Even the total of 2 million jobs over five years is fewer than Bill Clinton averaged every single year of his presidency, while shrinking the deficit.

What does this mean?

The Bush tax cuts have produced less than nothing. The economy is weaker for the effort. This is because those cuts have been targeted to the rich. The rich don't spend out of new income such as they get from tax refunds, but rather out of accumulated wealth.

It also means George Bush does not know what he is doing. Wait, you say, Dubya knows exactly what he is doing -- He is operating fiscal policy for the benefit of his rich corporate buddies. Fair point. What Bush does not know is that in the process he is killing the economy for everyone and choking off any possibilities for a rebound with big new debt.

He invaded Iraq with a purpose, too, but without understanding reality or the ramifications of his adventure. He and his Neocon ditto tank have produced a situation without an answer in the Middle East. They may have done the same thing with the domestic economy.

As Robert Rubin pointed out last week, the US -- alone among industrial nations -- has combined huge federal deficits and stagnant incomes with a very low personal savings, high personal debt and enormous trade deficits.

Yes, I am the voice of doom and gloom. It may surprise you that the economy of these posts is different than that witnessed to by the talking heads. It surprises me as well. Economics is not in the height of its glory right now, but surely we can do better than the line by Laurence J. Peter: "An economist is an expert who can explain precisely tomorrow why the things he predicted yesterday didn't happen today."

Most of the problem is politicization, both internal academic politics and the Heritage Foundation style. A new report from scientists at Emory University studied committed political partisans with MRIs. They discovered that reasoning centers in the brain were quiescent during the process of evaluating politically charged material, but circuits lit up that are connected with emotion and resolving conflicts. When acceptable conclusions were reached -- often by suppressing or ignoring difficult information -- circuits associated with behavior reward came on line. "Much like that seen when addicts get a drug," according to Drew Westen, director of clinical psychology at Emory. (See "Partisans don't let the facts get in the way of the truth.")

If you've ever seen economists argue, you know this is what is happening. Entire schools are built on logical flaws or assumption errors, supported only by vigorous debate and polemics. Very much too bad.

Thursday, January 26, 2006

Tacoma tax plan needs a shot

A couple of days ago I interviewed for a seat on the task force being set up by the Tacoma city council to investigate and analyze city manager Eric Anderson’s city services tax scheme. It wasn’t too long ago on the opinion page of the Tacoma Weekly that I was roundly criticizing Anderson and his plan and the horse he rode in on.

Things change. Anderson’s presentation has changed for one. He’s dropped the "user fee" tag he began with and now he calls it a tax. It is a tax. He’s dropped the occupancy part, so it is no longer subject to criticism as a poll tax.

And I changed. I have a new appreciation for a voter approved tax dedicated to the core missions of city government. Police, fire and libraries comprise the main business of city government, and it is these services that are most directly threatened by the current flimsy revenue architecture.

So far as I know, this is the only forward looking plan in the state to address the inevitable funding shortages to come. If anyone else is aware, please let me know. Otherwise it appears cities are willing to watch doe-eyed as their services come under the knife year after year. Tacoma will be opening the door for all cities if the plan goes through, because its implementation will require state approval. The state needs to approve any new forms of local taxation. That step is part of what will be a difficult road.

The shortfalls we face are, of course, the handiwork and the something-for-nothing right wing and their tax-cut initiatives. We are witnessing the same dynamic on the national stage, where an enormous new tower of debt is being built, a tower which is more and more unstable and which threatens to collapse on our futures, all so tax cuts can continue for the rich.

Locally we don’t have the option of constructing such a tower, since states and municipal governments are required to balance their budgets. This means if we tell the city to cut taxes, we tell the city to cut services. Our kids may not get the schools and police and parks they need, but the tax bills they get from us in twenty years will be entirely federal.

This city services tax is a way of making things, as they say, "transparent." Voters get to choose whether to have the appropriate level of services or not. Increases to the baseline level of revenue would be submitted in a periodic referendum, probably synchronized with the budget cycle.

Eyman and his cohorts ought to love this voter inut, but they won’t. They are in the business of bashing a vague "big government." They are not in the business of making the painful choices that follow when people buy their fiscal snake oil. For that they employ the simple if disingenuous tactic of denial. And then they leave it to the bureaucrats and politicians to do the dirty work.

One valid complaint heard from many citizens is they don’t want to give up their representative government. We hired these officials to make these decisions, they say, not to put them up for voter micromanagement. It’s a good point, but at least it could be an object lesson and a wake-up call. Taxes are simply the financing for public goods. You can’t have the goods without the taxes.

Let’s give Anderson’s idea a fair hearing and tweak it if it needs tweaking. There are dozens of complexities and a couple of potential dead-ends that need to be examined. But before that there are also misconceptions to be eliminated, and not left to stew for months and confuse public discussion. The following points ought to be broadcast to a wary public at the beginning of the process:

1. Your regular property tax bill will go down.

2. Your utility bill will go down.

3. You will get a new bill, possibly every other month.

4. No government agencies, no schools, no park districts will be taxed.

But first! Even before that! If I get chosen, I will force (by filibuster if necessary, so watch out!) a change in the name of the tax. "City services tax" is not right. It is not a tax on city services, like a utility tax is a tax on utilities, or an income tax is a tax on income. This would be a tax based on property value for the benefit of city services. I like "city services assessment," differentiating it from the bi-yearly bill, which would be a "parks and schools assessment." Besides "assessment" is more alliterative.

Things change. Anderson’s presentation has changed for one. He’s dropped the "user fee" tag he began with and now he calls it a tax. It is a tax. He’s dropped the occupancy part, so it is no longer subject to criticism as a poll tax.

And I changed. I have a new appreciation for a voter approved tax dedicated to the core missions of city government. Police, fire and libraries comprise the main business of city government, and it is these services that are most directly threatened by the current flimsy revenue architecture.

So far as I know, this is the only forward looking plan in the state to address the inevitable funding shortages to come. If anyone else is aware, please let me know. Otherwise it appears cities are willing to watch doe-eyed as their services come under the knife year after year. Tacoma will be opening the door for all cities if the plan goes through, because its implementation will require state approval. The state needs to approve any new forms of local taxation. That step is part of what will be a difficult road.

The shortfalls we face are, of course, the handiwork and the something-for-nothing right wing and their tax-cut initiatives. We are witnessing the same dynamic on the national stage, where an enormous new tower of debt is being built, a tower which is more and more unstable and which threatens to collapse on our futures, all so tax cuts can continue for the rich.

Locally we don’t have the option of constructing such a tower, since states and municipal governments are required to balance their budgets. This means if we tell the city to cut taxes, we tell the city to cut services. Our kids may not get the schools and police and parks they need, but the tax bills they get from us in twenty years will be entirely federal.

This city services tax is a way of making things, as they say, "transparent." Voters get to choose whether to have the appropriate level of services or not. Increases to the baseline level of revenue would be submitted in a periodic referendum, probably synchronized with the budget cycle.

Eyman and his cohorts ought to love this voter inut, but they won’t. They are in the business of bashing a vague "big government." They are not in the business of making the painful choices that follow when people buy their fiscal snake oil. For that they employ the simple if disingenuous tactic of denial. And then they leave it to the bureaucrats and politicians to do the dirty work.

One valid complaint heard from many citizens is they don’t want to give up their representative government. We hired these officials to make these decisions, they say, not to put them up for voter micromanagement. It’s a good point, but at least it could be an object lesson and a wake-up call. Taxes are simply the financing for public goods. You can’t have the goods without the taxes.

Let’s give Anderson’s idea a fair hearing and tweak it if it needs tweaking. There are dozens of complexities and a couple of potential dead-ends that need to be examined. But before that there are also misconceptions to be eliminated, and not left to stew for months and confuse public discussion. The following points ought to be broadcast to a wary public at the beginning of the process:

1. Your regular property tax bill will go down.

2. Your utility bill will go down.

3. You will get a new bill, possibly every other month.

4. No government agencies, no schools, no park districts will be taxed.

But first! Even before that! If I get chosen, I will force (by filibuster if necessary, so watch out!) a change in the name of the tax. "City services tax" is not right. It is not a tax on city services, like a utility tax is a tax on utilities, or an income tax is a tax on income. This would be a tax based on property value for the benefit of city services. I like "city services assessment," differentiating it from the bi-yearly bill, which would be a "parks and schools assessment." Besides "assessment" is more alliterative.

Wednesday, January 25, 2006

The economic model is broken

"A substantial amount has been done for the baseball and football teams. I'm here personally to find out whether the same is being considered fairly for the NBA,"

NBA Commissioner David Stern before the Senate Ways and Means Committee on Thursday.

It's a tag team match! Yes, the Seahawks' billionaire owner got a new stadium, and before that the Mariners' billionaire owner got a new stadium, but before that there was a mega-million dollar remake of the Sonics' home. Heck, the bonds on the Key (funny how they forgot the name) aren't even paid off. The fans and the taxpayers are getting the stuffing beaten out of them, and now we're supposed to feel guilty?

Seattle is not alone. The same edition of the Seattle Times that had Stern in the Local section had an article in Sports with the header "Blazers future uncertain." According to Portland Trailblazer owner Paul Allen's spokesman Lance Conn "all options are on the table" because "the economic model is broken."

Yes, the economic model is broken! We're paying players and coaches literally millions of dollars a year and now we're supposed to pony up to build better suites for high rollers. It is just absurd.

It's the worst of all economic models, a monopoly run by millionaires where cities are manipulated into a financing contest with each other. "The team can't win unless we've got the money." Phooey. Let them play the game on the court, not in our wallets.

Restaurants are already taxed on everything that moves and some things that don't. Sales tax, B&O tax, lots of payroll taxes, syrup taxes, alcohol taxes, and probably some I don't remember. Meanwhile Ray Allen pays the same state tax on his $14.5 million salary (team total is $52 million) as the minimum wage busboy. The corporate honchos who rent the fancy new suites get a deduction. Even Key Bank writes off the cost of paying to put its name on the place.

If they really end up taking the team to Kansas City, I have an idea. A new league. Seattle, Tacoma, Portland, Spokane, Fresno, Boise, San Jose. A cities group sells franchises for, say, a million. The maximum public investment is set, so big markets can't play George Steinbrenner and break the small markets. Maybe a salary scale for players is included.

And then we play basketball. What a concept.

We might even be able to watch people like Wil Conroy and Tre Simmons without having to go to Fargo or Marseilles.

FYI, there was one coherent voice in the house at the Ways & Means Committee.

Message Testimony of SEIU 775 President David Rolf

Senate Ways and Means

Members of the committee, my name is David Rolf. I am the President of SEIU 775, with 30,000 members in the long-term care industry, in every zip code in the state.

I cannot imagine a lower priority for the use of the public's money then the purpose this bill anticipates.

This contemplated act of corporate welfare takes place within the following context:

Incomes are stagnant or declining for 2/3 of households. Health care costs are eating up a greater percentage of employee paychecks and employer profits, even while benefits get cut and hundreds of thousands are uninsured. The average home price is now out of reach for an average income family in Seattle . Tuition costs put higher education out of reach for some working families. Fifty-two percent of all baby boomers have no retirement savings besides social security and their home equity. And, of course, the impoverishment of nursing home and home care workers threatens the quality of care for tens of thousands of elderly and disabled Washingtonians. The profitability of a sports facility should not be a higher priority than the health care of frail elderly people, or education, or housing.

The indirect transfer of public wealth to private, for-profit sports teams should not be a priority of our government, under any circumstances, at any time.

If you do pass this bill, we urge you to authorize the use of this tax for housing, health care, arts, education, and social services, but not to help subsidize the profitability of professional sports teams.

Thank you.

NBA Commissioner David Stern before the Senate Ways and Means Committee on Thursday.

It's a tag team match! Yes, the Seahawks' billionaire owner got a new stadium, and before that the Mariners' billionaire owner got a new stadium, but before that there was a mega-million dollar remake of the Sonics' home. Heck, the bonds on the Key (funny how they forgot the name) aren't even paid off. The fans and the taxpayers are getting the stuffing beaten out of them, and now we're supposed to feel guilty?

Seattle is not alone. The same edition of the Seattle Times that had Stern in the Local section had an article in Sports with the header "Blazers future uncertain." According to Portland Trailblazer owner Paul Allen's spokesman Lance Conn "all options are on the table" because "the economic model is broken."

Yes, the economic model is broken! We're paying players and coaches literally millions of dollars a year and now we're supposed to pony up to build better suites for high rollers. It is just absurd.

It's the worst of all economic models, a monopoly run by millionaires where cities are manipulated into a financing contest with each other. "The team can't win unless we've got the money." Phooey. Let them play the game on the court, not in our wallets.

Restaurants are already taxed on everything that moves and some things that don't. Sales tax, B&O tax, lots of payroll taxes, syrup taxes, alcohol taxes, and probably some I don't remember. Meanwhile Ray Allen pays the same state tax on his $14.5 million salary (team total is $52 million) as the minimum wage busboy. The corporate honchos who rent the fancy new suites get a deduction. Even Key Bank writes off the cost of paying to put its name on the place.

If they really end up taking the team to Kansas City, I have an idea. A new league. Seattle, Tacoma, Portland, Spokane, Fresno, Boise, San Jose. A cities group sells franchises for, say, a million. The maximum public investment is set, so big markets can't play George Steinbrenner and break the small markets. Maybe a salary scale for players is included.

And then we play basketball. What a concept.

We might even be able to watch people like Wil Conroy and Tre Simmons without having to go to Fargo or Marseilles.

FYI, there was one coherent voice in the house at the Ways & Means Committee.

Message Testimony of SEIU 775 President David Rolf

Senate Ways and Means

Members of the committee, my name is David Rolf. I am the President of SEIU 775, with 30,000 members in the long-term care industry, in every zip code in the state.

I cannot imagine a lower priority for the use of the public's money then the purpose this bill anticipates.

This contemplated act of corporate welfare takes place within the following context:

Incomes are stagnant or declining for 2/3 of households. Health care costs are eating up a greater percentage of employee paychecks and employer profits, even while benefits get cut and hundreds of thousands are uninsured. The average home price is now out of reach for an average income family in Seattle . Tuition costs put higher education out of reach for some working families. Fifty-two percent of all baby boomers have no retirement savings besides social security and their home equity. And, of course, the impoverishment of nursing home and home care workers threatens the quality of care for tens of thousands of elderly and disabled Washingtonians. The profitability of a sports facility should not be a higher priority than the health care of frail elderly people, or education, or housing.

The indirect transfer of public wealth to private, for-profit sports teams should not be a priority of our government, under any circumstances, at any time.

If you do pass this bill, we urge you to authorize the use of this tax for housing, health care, arts, education, and social services, but not to help subsidize the profitability of professional sports teams.

Thank you.

Rubin's Rx

Clinton's economic guru, former Treasury secretary Robert Rubin, wrote a piece in Tuesday's Wall Street Journal on what's up with the economy. "Rubinomics," you will remember, was widely credited with turning things around under Clinton. It concentrated on a return to fiscal fundamentals, deficit reduction, targeted tax breaks, open markets, and social spending on education and against poverty. His piece today continued on the same line. (Why not?)

Rubin says (in my translation, see below):

We are in deep do-do, and the Supply Side nonsense that things are going to turn around is bull.

Big deficits cannot be tolerated, since we are facing big payouts in entitlements, exorbitant health care costs, and years of underfunding education. Medicare is several times as great a problem as Social Security.

Our fiscal problems are made worse because the U.S., alone among the developed nations, has combined them with very low personal savings rates, high personal debt, and enormous trade deficits -- currently over 6% of GDP -- stemming partly from our budget deficits. [It is fair to note here that trade deficits were not much better under Clinton/Rubin.]

We can close more than three-quarters of the deficit by rescinding the tax breaks for the rich. There is no other practical means.

The current illusion of strength in the economy comes from the housing boom, which was generated by low interest rates. Low interest rates have come from (1) Greenspan rolling over for W like he never did for Bill and me, (2) foreign central banks propping up the dollar for their own trade purposes, and (3) lack of demand for capital from business (not a good thing). Interest rates will go up soon, largely because federal deficits are going to bid them up.

We need significant new public investment, both to turn around the decline in people's incomes and to equip our citizens to participate in economic growth.

Global integration, including all nations, must continue. Essential to its success is reducing global poverty. Further integration will be politically possible only if everybody is "participating" here at home, as above. It is problemmatic that who want global integration do not support the significant domestic investment needed to get people participating on a broad scale, and those who want the domestic investment on people are not so sure about globalization.

End of translation, you saved 745 words.

Rubin has experience turning bad situation around, although he and Clinton did have a couple of breaks not available today. For example, when they cut the deficit and interest rates fell, a huge re-fi boom followed. This will not happen again; interest rates are already low and all the re-fi-ing has been done. And oil prices fell for Clinton and Rubin, then stayed low, and fell some more before rising a bit at the end. Low oil prices are no longer on the horizon. Also, the technology boom was probably not entirely invented by the Clinton or his vice president.

I was impressed particularly by Rubin's call for broad public investment to first develop human and physical capital, but also to get people's incomes going up again. The likelihood of such a program is dim at best, even under a Democrat. The return to fundamentals in the first year of the Clinton administration was far from painless. The modest tax increase it required cost Democrats control of Congress. (Recall that Maria Cantwell's yes vote cost her a second term in the House, when she was defeated by anti-tax demagoguery.)

But it would work.

Translator's technical notes:

One thing I didn't know about Rubin is he has a very abstruse style of writing. While he is not purposefully ambiguous as is Alan Greenspan, it is very thick. The following examples depict how the original text has been transposed into blogish.

The title "We Must Change Policy Direction," to "Change Policy!"

A sample paragraph: "Re-establishing seriousness of purpose regarding economic policy and acting to meet the challenges of our era will require our political system to do what it is not doing today: making choices that are very difficult politically, compromising among divergent views in order to reach common ground, and putting aside ideology in favor of facts and analysis."

This paragraph was omitted as superfluous. Had it been included, it would have read, "We need to get together, face facts and show some backbone before it is too late."

Mine is simply an aggressive rendition of Rubin's opinions. They are not my own, even if there are some similarities.

Rubin says (in my translation, see below):

We are in deep do-do, and the Supply Side nonsense that things are going to turn around is bull.

Big deficits cannot be tolerated, since we are facing big payouts in entitlements, exorbitant health care costs, and years of underfunding education. Medicare is several times as great a problem as Social Security.

Our fiscal problems are made worse because the U.S., alone among the developed nations, has combined them with very low personal savings rates, high personal debt, and enormous trade deficits -- currently over 6% of GDP -- stemming partly from our budget deficits. [It is fair to note here that trade deficits were not much better under Clinton/Rubin.]

We can close more than three-quarters of the deficit by rescinding the tax breaks for the rich. There is no other practical means.

The current illusion of strength in the economy comes from the housing boom, which was generated by low interest rates. Low interest rates have come from (1) Greenspan rolling over for W like he never did for Bill and me, (2) foreign central banks propping up the dollar for their own trade purposes, and (3) lack of demand for capital from business (not a good thing). Interest rates will go up soon, largely because federal deficits are going to bid them up.

We need significant new public investment, both to turn around the decline in people's incomes and to equip our citizens to participate in economic growth.

Global integration, including all nations, must continue. Essential to its success is reducing global poverty. Further integration will be politically possible only if everybody is "participating" here at home, as above. It is problemmatic that who want global integration do not support the significant domestic investment needed to get people participating on a broad scale, and those who want the domestic investment on people are not so sure about globalization.

End of translation, you saved 745 words.

Rubin has experience turning bad situation around, although he and Clinton did have a couple of breaks not available today. For example, when they cut the deficit and interest rates fell, a huge re-fi boom followed. This will not happen again; interest rates are already low and all the re-fi-ing has been done. And oil prices fell for Clinton and Rubin, then stayed low, and fell some more before rising a bit at the end. Low oil prices are no longer on the horizon. Also, the technology boom was probably not entirely invented by the Clinton or his vice president.

I was impressed particularly by Rubin's call for broad public investment to first develop human and physical capital, but also to get people's incomes going up again. The likelihood of such a program is dim at best, even under a Democrat. The return to fundamentals in the first year of the Clinton administration was far from painless. The modest tax increase it required cost Democrats control of Congress. (Recall that Maria Cantwell's yes vote cost her a second term in the House, when she was defeated by anti-tax demagoguery.)

But it would work.

Translator's technical notes:

One thing I didn't know about Rubin is he has a very abstruse style of writing. While he is not purposefully ambiguous as is Alan Greenspan, it is very thick. The following examples depict how the original text has been transposed into blogish.

The title "We Must Change Policy Direction," to "Change Policy!"

A sample paragraph: "Re-establishing seriousness of purpose regarding economic policy and acting to meet the challenges of our era will require our political system to do what it is not doing today: making choices that are very difficult politically, compromising among divergent views in order to reach common ground, and putting aside ideology in favor of facts and analysis."

This paragraph was omitted as superfluous. Had it been included, it would have read, "We need to get together, face facts and show some backbone before it is too late."

Mine is simply an aggressive rendition of Rubin's opinions. They are not my own, even if there are some similarities.

Tuesday, January 24, 2006

A jobless recovery is not a recovery III

Full employment was once the primary objective of presidential economic policy. It was required by law, mandated by Congress in 1946 under Harry Truman in the Full Employment Act. That Act required an annual report to describe what the president was doing to achieve this end. This report, The Economic Report of the President, is still a terrific source of data, but it has lost its focus on jobs and has become little more than repository for failed predictions.

In 1946, the object lessons of the Great Depression and then World War II were fresh in the minds of the people and their lawmakers. They knew that the Depression was only the deepest in a series of crippling troughs that had afflicted the prewar capitalist economy. Previously these events were called "panics." (The much milder downturns subsequent to World War II have been termed "recessions.") But the Great Depression was the formational event of generations.

The economics of this period was energized by three things: the development of Demand Side economics under John Maynard Keynes (KANES), the commitment of many of the most capable minds of the era to solving the social pandemic of Depressions, and the patent fact that the successful economies of the 1930s were those of Nazi Germany and Stalinist Russia.

The economic discipline suggested by Keynes, which is now considered so left wing, actually delivered capitalism from its own internal contradictions. The mobilization of the country during World War II demonstrated beyond a doubt that government action and organization could effectively focus the apparently uncontrollable energies of a capitalistic market economy.

What emerged from the Depression and the War has been called welfare capitalism or social capitalism. It was not the unfettered capitalism of pre-Depression years, but capitalism nonetheless. To be clear, though he was a prominent figure in political circles, and an able advocate, no country implemented Keynes' prescriptions as a blueprint, not even Britain. Roosevelt's New Deal was more an American invention than a knock-off of the British economist's ideas. To demonstrate his reach, however, realize that prior to Keynes macroeconomics did not even exist conceptually.

The Americans, followers of Keynes and others, who schooled themselves on the Depression and instituted the New Deal, were key players in the financing and industrial organization of World War II. They then managed a very dicey transition back to peacetime. After that they sponsored a postwar economics focused on jobs, and won the peace with the Marshall Plan to rebuild Europe (arguably saving democracy and capitalism there). From this period arose the steady trend line in growth we now take for granted. (We take more or less steady growth for granted even though it has not been the experience for half of our population for the past 25 years.)

Richard Nixon said in 1972, "We're all Keynesians now." Since the moment he spoke the words, they have become less and less true. The stagflation of the 1970s, the Supply Side debacle of the 1980s, even the return to fundamentals under Clinton and Rubin in the 1990s, and especially the bullshit first, ask questions later, policies of George II, have left us adrift in a confusion of laissez faire combined with corporatism that allows only tinkering at the margins.

The successful economy of the 1950s and 1960s and 1970s has gradually been left behind. Calling the current US economy successful when its citizens are hungry, cold, sick without care, homeless, uneducated, clinging to meaningless jobs, unable to meet clear and obvious environmental challenges, uncertain of their futures, is simply sick. The class structure that has emerged and now demands dominance is not a necessary evil to promote dynamic markets. It is simply decadence and decay.

The successful economies are those of Scandinavia, where 50 percent of GDP goes to taxes, and the government is a true partner with business and labor. That 50 percent includes true social security with health care, plus other high-value public goods, including government sponsored R&D that helps business. (Helping business in America means tax giveaways to the rich and powerful.) Even to dream of this system is impossible in the political and economic climate of modern America.

We sit at a crisis point in the governance of the country, a crisis point in the ecological life of the planet, and a crisis point in the social welfare of our society. We see education, energy, transportation, health care, the environment as burdens too heavy for our aging population. We experience a globalization captured by corporate powers and have little idea of what to do about it but object. We hear a lot about the information economy, and the needs of the new technical age, and looking forward is essential. But equally important is to reform the old technologies and systems, to rid ourselves of the entrenched corporatism that controls them, and to regain control of the government, with its disastrous incompetence and cronyism, they have put in power.

The magic of the 1990s was new industries, the tech industries, that demanded skilled workers and created an upward mobility that refreshed everything. Rational work-first economics is still viable. It requires appropriate valuation of public goods such as education, environmental balance, public health, etc., and the willingness to structure government and the market accordingly. These many challenges can be the very engines of growth, if we but define value and then create and realize that value by putting people to work.

That would be a recovery.

In 1946, the object lessons of the Great Depression and then World War II were fresh in the minds of the people and their lawmakers. They knew that the Depression was only the deepest in a series of crippling troughs that had afflicted the prewar capitalist economy. Previously these events were called "panics." (The much milder downturns subsequent to World War II have been termed "recessions.") But the Great Depression was the formational event of generations.

The economics of this period was energized by three things: the development of Demand Side economics under John Maynard Keynes (KANES), the commitment of many of the most capable minds of the era to solving the social pandemic of Depressions, and the patent fact that the successful economies of the 1930s were those of Nazi Germany and Stalinist Russia.

The economic discipline suggested by Keynes, which is now considered so left wing, actually delivered capitalism from its own internal contradictions. The mobilization of the country during World War II demonstrated beyond a doubt that government action and organization could effectively focus the apparently uncontrollable energies of a capitalistic market economy.

What emerged from the Depression and the War has been called welfare capitalism or social capitalism. It was not the unfettered capitalism of pre-Depression years, but capitalism nonetheless. To be clear, though he was a prominent figure in political circles, and an able advocate, no country implemented Keynes' prescriptions as a blueprint, not even Britain. Roosevelt's New Deal was more an American invention than a knock-off of the British economist's ideas. To demonstrate his reach, however, realize that prior to Keynes macroeconomics did not even exist conceptually.

The Americans, followers of Keynes and others, who schooled themselves on the Depression and instituted the New Deal, were key players in the financing and industrial organization of World War II. They then managed a very dicey transition back to peacetime. After that they sponsored a postwar economics focused on jobs, and won the peace with the Marshall Plan to rebuild Europe (arguably saving democracy and capitalism there). From this period arose the steady trend line in growth we now take for granted. (We take more or less steady growth for granted even though it has not been the experience for half of our population for the past 25 years.)

Richard Nixon said in 1972, "We're all Keynesians now." Since the moment he spoke the words, they have become less and less true. The stagflation of the 1970s, the Supply Side debacle of the 1980s, even the return to fundamentals under Clinton and Rubin in the 1990s, and especially the bullshit first, ask questions later, policies of George II, have left us adrift in a confusion of laissez faire combined with corporatism that allows only tinkering at the margins.

The successful economy of the 1950s and 1960s and 1970s has gradually been left behind. Calling the current US economy successful when its citizens are hungry, cold, sick without care, homeless, uneducated, clinging to meaningless jobs, unable to meet clear and obvious environmental challenges, uncertain of their futures, is simply sick. The class structure that has emerged and now demands dominance is not a necessary evil to promote dynamic markets. It is simply decadence and decay.

The successful economies are those of Scandinavia, where 50 percent of GDP goes to taxes, and the government is a true partner with business and labor. That 50 percent includes true social security with health care, plus other high-value public goods, including government sponsored R&D that helps business. (Helping business in America means tax giveaways to the rich and powerful.) Even to dream of this system is impossible in the political and economic climate of modern America.

We sit at a crisis point in the governance of the country, a crisis point in the ecological life of the planet, and a crisis point in the social welfare of our society. We see education, energy, transportation, health care, the environment as burdens too heavy for our aging population. We experience a globalization captured by corporate powers and have little idea of what to do about it but object. We hear a lot about the information economy, and the needs of the new technical age, and looking forward is essential. But equally important is to reform the old technologies and systems, to rid ourselves of the entrenched corporatism that controls them, and to regain control of the government, with its disastrous incompetence and cronyism, they have put in power.

The magic of the 1990s was new industries, the tech industries, that demanded skilled workers and created an upward mobility that refreshed everything. Rational work-first economics is still viable. It requires appropriate valuation of public goods such as education, environmental balance, public health, etc., and the willingness to structure government and the market accordingly. These many challenges can be the very engines of growth, if we but define value and then create and realize that value by putting people to work.

That would be a recovery.

Saturday, January 21, 2006

A jobless recovery is not a recovery II

Employment growth is the best simple measure to watch in judging economic well-being. GDP is misleading. It describes the agitation of a market economy and includes borrowing as earning. We covered that last week. Employment is better. Aside from the obvious benefits to job holders and their families, which ought to be a primary consideration, job growth is closely related to investment, balanced budgets, falling poverty levels and other measures.

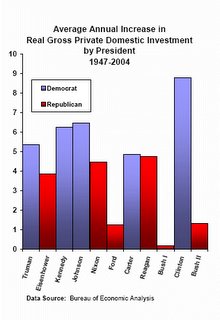

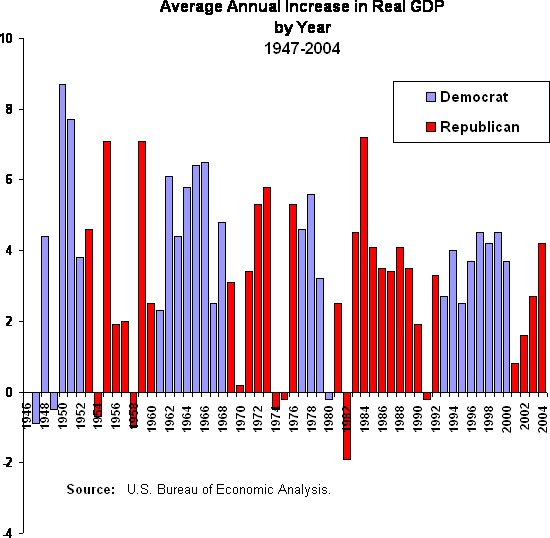

The following charts describe economic performance by president. (I am pressing them into service for the present discussion because they're what I have at hand. ) We can assume that presidents determine economic policy and that Democrats are more bottom up vs. Republicans top down.)

First, notice the correlation between investment and employment. Employment growth and investment are mutually reinforcing and create a productive cycle of growth. Investment creates jobs which creates demand which stimulates production and more investment, which creates jobs which stimulates.... You could begin with jobs create demand which stimulates production and investment.... Or demand stimulates production and investment which creates jobs which stimulates....

This last was the genius of Keynesian fiscal stimulus. It has been bastardized by the current administration to read tax cuts for the rich are good for the economy. In fact, tax cuts for the rich do not create demand because the rich spend out of accumulated wealth, not out of new income, which they just put in the bank. The same money to the poor or middle class -- boom! The sonic barrier. Cuts to social programs are patently inefficient economically.

It is a cycle. One element cannot be isolated and glorified to the exclusion of the other elements. Trickle down economics has attempted to isolate investment through investment tax breaks and preferences to savings. Insofar as these reduce demand from other sources or jobs, the experience is frustration. Witness the abysmal performance of Supply Side measures under Reagan. I do understand that all investment is not created equal. Investment in palatial residences will not yield the same long-term benefits as, say, investment in energy technology.

Next, notice the absence of a relationship between the unemployment rate and employment. The unemployment rate is calculated as the number of unemployed people looking for work as a percentage of the total civilian labor force. The labor force expands when there are good jobs to be had, and it contracts when there are no jobs worth having. People go to school, go on disability, go underground, hang out, become "discouraged workers," etc.

This expands and contracts the denominator, which makes a weak measure that unfortunately has been relied on too much. The Fed, for example, treats the unemployment rate as sensitive indicator of impending inflation, which it is not.

(To be fair, see that these numbers are through 2004. I guess W is finally on the positive side in terms of creating jobs. New annual numbers are out next month.)

Just so we cover it, and assume that employment growth means bad news for profits, notice that profits are steady in all weather -- as a percentage of total income. The implication of this "as a percentage" is that Democrats and stronger growth mean a stronger bottom line in absolute terms as well. The fascination of corporations for Republicans has more to do with CEOs and managers and an insider control mentality than it does for all shareholders' interests.

The business community seems to be captive to the Republicans, even small businesses, though I suspect it is more the organizations that purport to represent these folks that are in the Republican camp (easier to lobby for tax breaks than sound economics?). But look again at the jobs numbers when you hear, "Being a successful businessman, I know how to create jobs." Entrepreneurs are in the business of identifying opportunities for investment, which means potential demand. Investment can be stimulated by technical innovation or pressing public need or other factors. Jobs are created by the cycle of investment and demand as identified above.

Now, see how GDP is stronger under Democrats, but kind of respectable under Republicans. This is because -- thump -- a lot of that GDP under the GOP is generated by borrowing. I posted the federal borrowing chart last week, as well as a measure unique to me called "Net GDP," which was GDP minus federal borrowing, what GDP would have done without the borrowing. If you look that one up, you will see its similarity to the two charts at the top. Federal borrowing as a short-term stimulus effort is okay. It cannot become a way of life, as it has under Republican administrations.

Finally, in a chart that is not going to come through very well on the blog, but I find in my tedious way extremely fascinating is the unemployment rate year over year. I know I just panned the unemployment rate as flaccid and weak on fundamentals. But look, under Democrats the unemployment rate goes down, like stair steps, consistently, no matter what other evens are going on, no matter how many new job-seekers come into the market. (Exceptions, 1948, when Truman had to deal with 9 million men and women returning from service in the War, and in 1980, when Volcker panicked and restricted the money supply and Carter choked under the Iran crisis.) No matter how big the denominator gets, the numerator outpaces it. Very cool.

Debt, monetizing debt, lying about debt

The Senate voted to lift the debt limit by $781 billion last Thursday. Total debt is up to nearly $9 trillion. The Bush deficits keep adding to the pile. As big as they are, they are still being understated. Official numbers on the deficit depend on a continuing back door into Social Security Funds.

It's not that I mind filling Social Security Retirement and other funds with federal bonds. What I mind is the bankrupting of the operating budget by incompetence and lying and then concealing the extent of the crime. The level of borrowing is an important measure of solvency. A bond is a debt instrument. Claiming we're not borrowing when we are is a fraud.

I also mind the hoopla of a couple of Republican Senators objecting to this casino financing in the name of fiscal responsibility. This is strictly a show for the benefit of the folks back home. Big debt and Republicans go together (see chart).

The great preponderance of debt, as you can see, has been incurred during the stewardship of Republican presidents.

This is business as usual for them. Much like John Ashcroft showing up behind the desk of his own K street lobbying firm is business as usual.

A NYT story says that in an hour long interview, "Mr. Ashcroft used the word ‘integrity' scores of times." )

Integrity for Ashcroft is similar to fiscal responsibility for Republicans as a party, just labels on marketing props, not actual codes of conduct. The amount we owe has now ballooned to such an extent that, along with the impending expansion of Social Security and Medicare and the unwillingness of the GOP to face facts, the continued solvency of the federal government has come into question.

Will we be able to raise taxes to the level needed to pay off these debts and meet our entitlement obligations at the same time? Particularly when the party putting on the show is the hate-taxes party? Some financial advisors and economic observers have begun talking openly about "monetizing the debt."

"Monetizing the debt" is lingo for using the printing press to pay off bonds. It's an act of desperation. Obviously it is not expected by investors, because US government bonds are still trading at a high price. But they should worry. The security and liquidity of government bonds, which is why they are trading at such a price, is not guaranteed.

Most folks worry about inflation, which is inevitable with monetizing debt. I worry about default, or a "change in terms," where bonds are not paid as promised, but on an "adjusted schedule." After all, the printing presses are in control of the bankers, the Federal Reserve being the central bank. Bankers hate inflation. Screws up their interest rate calculations. Or it could be a combination.

Whatever happens won't be pretty. These are financial stresses never before seen, and the fallout will be both domestic and international.

But what else do we do? We are incurring debt at a sickening rate. Pretty soon money is going to cost more. Rising interest rates will mean a slowing domestic economy and higher debt service for the government.

In ten or fifteen years (no, not tomorrow), or when the cracks become apparent, we're into the deep doo-doo. In the Clinton era, Rubinomics combined with very low energy prices gave us the break we needed. Unfortunately, we didn't take advantage of it.

# Posted by Alan : 9:48 PM

It's not that I mind filling Social Security Retirement and other funds with federal bonds. What I mind is the bankrupting of the operating budget by incompetence and lying and then concealing the extent of the crime. The level of borrowing is an important measure of solvency. A bond is a debt instrument. Claiming we're not borrowing when we are is a fraud.

I also mind the hoopla of a couple of Republican Senators objecting to this casino financing in the name of fiscal responsibility. This is strictly a show for the benefit of the folks back home. Big debt and Republicans go together (see chart).

The great preponderance of debt, as you can see, has been incurred during the stewardship of Republican presidents.

This is business as usual for them. Much like John Ashcroft showing up behind the desk of his own K street lobbying firm is business as usual.

A NYT story says that in an hour long interview, "Mr. Ashcroft used the word ‘integrity' scores of times." )

Integrity for Ashcroft is similar to fiscal responsibility for Republicans as a party, just labels on marketing props, not actual codes of conduct. The amount we owe has now ballooned to such an extent that, along with the impending expansion of Social Security and Medicare and the unwillingness of the GOP to face facts, the continued solvency of the federal government has come into question.

Will we be able to raise taxes to the level needed to pay off these debts and meet our entitlement obligations at the same time? Particularly when the party putting on the show is the hate-taxes party? Some financial advisors and economic observers have begun talking openly about "monetizing the debt."

"Monetizing the debt" is lingo for using the printing press to pay off bonds. It's an act of desperation. Obviously it is not expected by investors, because US government bonds are still trading at a high price. But they should worry. The security and liquidity of government bonds, which is why they are trading at such a price, is not guaranteed.

Most folks worry about inflation, which is inevitable with monetizing debt. I worry about default, or a "change in terms," where bonds are not paid as promised, but on an "adjusted schedule." After all, the printing presses are in control of the bankers, the Federal Reserve being the central bank. Bankers hate inflation. Screws up their interest rate calculations. Or it could be a combination.

Whatever happens won't be pretty. These are financial stresses never before seen, and the fallout will be both domestic and international.

But what else do we do? We are incurring debt at a sickening rate. Pretty soon money is going to cost more. Rising interest rates will mean a slowing domestic economy and higher debt service for the government.

In ten or fifteen years (no, not tomorrow), or when the cracks become apparent, we're into the deep doo-doo. In the Clinton era, Rubinomics combined with very low energy prices gave us the break we needed. Unfortunately, we didn't take advantage of it.

# Posted by Alan : 9:48 PM

Thursday, January 19, 2006

Good news on midnight budget machinations

Southwest Washington's Rep. Brian Baird was understating it with "a shame, a disgrace, and an embarrassment that these critically important bills were brought up in the dead of the night, laden with unrelated provisions, and passed by sheep-like members who had but the slightest idea what was in them.”

The subject was the "martial law" gambit by which Congressional leaders evaded normal House rules for the budget reconciliation and defense appropriations bill and rushed through a 774 page report between midnight and 6:00 a.m. December 19, exactly one month ago. (The affair was lost a bit in the furor over ANWR drilling, foiled nicely, thank you, by our state's junior senator.)

“The people’s elected representatives deserve time to read and debate legislation that will have such an enormous impact on our national defense and domestic programs,” said Congressman Baird.

They didn't get it. The final vote on the reconciliation spending bill was taken after all of 40 minutes of debate. Never mind a monopoly on power, some things still need to be done in the middle of the night.

That is the bad news. We told you about it at the time. There is good news.

The Senate deleted some minor provisions and the bill has to go back to the House for another vote. This time there will be no confusion about what the legislation would do, and maybe some public accountability. The next vote may be as early as February 1.

The bill as it sits now:

- Increases in Medicaid co-payments and premiums, and reductions in Medicaid benefits (many affecting children), that total $16 billion over the next ten years, according to the Congressional Budget Office.

- Institutes substantial and controversial changes in welfare policy.

- Reduces in child support enforcement funding which would, according to CBO, mean $8.4 billion of child support over the next ten years will go uncollected.

- Delays certain SSI payments for up to a year for many poor individuals with disabilities who are found eligible for SSI.

- Changes federal foster care rules that will hamper states from supporting certain relatives who are raising children because the children’s parents are unable or unfit to do so.

- For the first time since Medicaid began, the conference agreement allows states to deny contraception to poor women. Family planning services are a mandatory under current Medicaid law.

- It drops key elements of the Senate bill that would have garnered substantial savings in the corporate exploitation Medicare and Medicaid programs.

- Abandons the Senate's preference to eliminate a $10 billion fund to encourage preferred provider organizations to participate in Medicare.

Tuesday, January 17, 2006

A jobless recovery is not a recovery Part I

We are told daily that GDP is up and our economy is moving forward, but we are working longer and harder just to keep up, and the quality of life seems to be deteriorating. EPI's snapshot this week shows real income has declined for most of us during the "recovery" of the past three years.

GDP is a bad measure of economic activity. It does not measure the health of the economy, nor the well-being of its citizens, only the agitation on the market side. Wars, crime, alcoholism -- the economy's "bads" -- count just as much as the "goods" of food and shelter.

Environmental damage is completely ignored. Actually, we count the clean-up in GDP, but the original damage? Didn't happen. Also see the current Bush defense of oil-based energy policy. No longer does he doubt the science of climate change, now he says our economy cannot afford to do anything about it. Bill Clinton has labeled the claim "flat wrong." (What happened to "Bull!"?) Clinton has, in fact, proposed an economic future for America based on the development of energy technology.

An alternative measure to GDP -- the Genuine Progress Indicator (GPI) -- which takes into account the facts on the ground is actually down more than 45% since 1975.

GDP counts borrowing as earning. And growing debt is the only explanation for the current rise in GDP. The value of goods purchased, added together, equals Gross Domestic Product. This is like adding your paycheck to your credit card balance and calling the total your earnings.

Am I just a loyal liberal footsoldier dissing the good news of GDP and exploiting the bad news of massive debt, falling incomes and tepid employment growth, all for the prurient interest of my fellow radic-libs? I don't think so.

I am more like the nonplussed Frenchman who objected to the US invasion of a Middle East country on flimsy pretext. When the adventure turned out to be a catastrophe, I was not surprised. The economy is similar. I'm just happy economist jokes are less offensive than French jokes.

The parallels are striking. The Bush-Cheney axis decides what they are going to do, and the facts and "official" rationale are relegated to the PR department, where they will be adjusted daily for public consumption. In Iraq, the "imminent threat of WMD" changed to "getting rid of Saddam" changed to "establishing democracy."

With tax cuts, Bush first promoted them "because it's your money" (talking about the surplus). Subsequently we learned it wasn't our money, after all, it was our kids' money. But, don't worry, it's not going to us anyway, it's going to the rich.

When things started to tank, tax cuts became "a necessary measure to help the economy after the terrorist attacks." This is, in fact, the line that sold Congress. Bull! One, 9-11 had a mild effect at most on the economic trajectory. Airlines, for example, suffered far more from fuel prices than from the temporary discouragement of travellers. Two, and more to the point, the Bush tax cuts and the shameless slicing away at our social and educational programs cannot help the economy. That policy gun is pointed 180 degrees away from the target. To improve spending and consumer confidence, and thus demand for domestic business, fiscal decisions should favor the middle and lower class, not the rich.

Now he says, "Stay the course." If we are lucky, the course is circular, because off the bow it looks like we are heading straight for the rocks.

Next time, a look at employment as an alternative measure of economic health.

GDP is a bad measure of economic activity. It does not measure the health of the economy, nor the well-being of its citizens, only the agitation on the market side. Wars, crime, alcoholism -- the economy's "bads" -- count just as much as the "goods" of food and shelter.

Environmental damage is completely ignored. Actually, we count the clean-up in GDP, but the original damage? Didn't happen. Also see the current Bush defense of oil-based energy policy. No longer does he doubt the science of climate change, now he says our economy cannot afford to do anything about it. Bill Clinton has labeled the claim "flat wrong." (What happened to "Bull!"?) Clinton has, in fact, proposed an economic future for America based on the development of energy technology.

An alternative measure to GDP -- the Genuine Progress Indicator (GPI) -- which takes into account the facts on the ground is actually down more than 45% since 1975.

GDP counts borrowing as earning. And growing debt is the only explanation for the current rise in GDP. The value of goods purchased, added together, equals Gross Domestic Product. This is like adding your paycheck to your credit card balance and calling the total your earnings.

Am I just a loyal liberal footsoldier dissing the good news of GDP and exploiting the bad news of massive debt, falling incomes and tepid employment growth, all for the prurient interest of my fellow radic-libs? I don't think so.

I am more like the nonplussed Frenchman who objected to the US invasion of a Middle East country on flimsy pretext. When the adventure turned out to be a catastrophe, I was not surprised. The economy is similar. I'm just happy economist jokes are less offensive than French jokes.

The parallels are striking. The Bush-Cheney axis decides what they are going to do, and the facts and "official" rationale are relegated to the PR department, where they will be adjusted daily for public consumption. In Iraq, the "imminent threat of WMD" changed to "getting rid of Saddam" changed to "establishing democracy."

With tax cuts, Bush first promoted them "because it's your money" (talking about the surplus). Subsequently we learned it wasn't our money, after all, it was our kids' money. But, don't worry, it's not going to us anyway, it's going to the rich.

When things started to tank, tax cuts became "a necessary measure to help the economy after the terrorist attacks." This is, in fact, the line that sold Congress. Bull! One, 9-11 had a mild effect at most on the economic trajectory. Airlines, for example, suffered far more from fuel prices than from the temporary discouragement of travellers. Two, and more to the point, the Bush tax cuts and the shameless slicing away at our social and educational programs cannot help the economy. That policy gun is pointed 180 degrees away from the target. To improve spending and consumer confidence, and thus demand for domestic business, fiscal decisions should favor the middle and lower class, not the rich.

Now he says, "Stay the course." If we are lucky, the course is circular, because off the bow it looks like we are heading straight for the rocks.

Next time, a look at employment as an alternative measure of economic health.

Sunday, January 15, 2006

Is China dumping the dollar?

Reported in the Washington Post and picked up at Daily Kos with much alarm was the apparent intent of China to move some of its foreign exchange reserves away from the dollar. (All this by way of Pacific Views.)

Why? What does it mean? John Campanelli at DKos says, "In sum, we're screwed." (It was more descriptive yesterday, but has apparently been edited down.)

This was and is inevitable. "Trade" is trade of goods through the medium of exchange, the currency. It is not trade of the currency for the goods. It is supposed to be goods for goods. China can't eat all the dollars it has absorbed in its years of trade surplus with the US.

Standard economic theory predicts that in situations of trade imbalance, the currencies' exchange rates will adjust, making the goods of the surplus country relatively more costly and those of the deficit country more cheap. Standard economic theory, so far as I know, does not have an answer to why this has begun only after 30 years of immense US trade deficits -- if it is even happening now.